Getting cheap car insurance is dependant on one's knowledge of available auto insurance options. This article takes a look at different auto insurance coverage options in detail so that it provides the necessary information to compare and shop for cheap auto insurance quotes in Florida for the right coverage and not just the mandatory cover of $10,000 PIP and $10,000 PDL. Do not be carried away by cheap insurance claims which peddle minimum covers. They are cheap for a reason. The art of cheap Florida auto insurance has more to do with understanding the actual coverage you would need when you need it (before an accident happens) without cutting corners. Striking a balance on coverage which is adequate while keeping it all affordable is what cheap Florida auto insurance is all about.

Medical Payment or Med-pay Coverage:

The minimum statutory insurance cover is neither adequate nor cheap if god forbid, you end up being in an incident. Costs multiply quickly even in a seemingly minor incident. The minimum statutory cover (PIP) guarantees swift medical help when needed, instead of trying to see who pays for what up to the permissible limit. But with the medical cost being what they are costs escalate quickly and the minimum is not adequate. You can buy additional/optional medical payment insurance. Med pay covers medical bills of the person insured, person’s family and other passengers, just as PIP coverage would pay. Coverage extends even if not in own car, as a bicycle rider, or a pedestrian, etc. If someone else drives the insured person’s car and has an accident, that person may be covered by med pay irrespective of whether a person has own med pay or not. Med pay will not pay for lost wages if in an incident, or maid service. This will be paid by PIP.

- Med pay will pay 20% co-pay which is not covered by the mandatory PIP cover.

- Sometimes Med pay will also pay PIP deductible for hospital costs.

- Med pay is not dependant on fault; it will pay even if you are at fault.

- Discuss coverage options and fine print with insurance co/agent for comparison.

Collision and Comprehensive Coverage:

Florida is a no-fault state, the mandatory Property damage of $10,000 will help pay damages you caused to others. But what happens when you are hit by someone else? You are at the mercy of the other party’s insurance company who might not respond to your need as quickly. It might end up being a long drawn process, with paperwork, investigations, etc. What if there is no police report filed? Collision coverage comes to your aid in such circumstances. Collision coverage applies to the following:

- If you are hit by another car

- You hit another car

- You hit any object like a wall, rock, etc.

- Single car Rollover

You can file a claim with your own company quickly so you are not stranded for lack of a car. Having a rental car at your disposal until the car is repaired will not disrupt your life. (Make sure this option is provided with the coverage when you shop) Getting to work, picking up and dropping off your kids, etc cannot stop just because you do not have a car right? Deductible: The collision deductible kicks in though so keep the deductible affordable and not too high which you cannot pay. A bit of what-if analysis will help you arrive at a deductible which will not break the bank or keep your premiums very high. Remember, your deductible should be an amount you can pay at all times easily. Your insurance company will take care of recovery from the other party. The insurance company will repair or pay up to the market value or fair value of the car minus the deductible which you will have to pay. Collision coverage is a must-have in Florida with a high incidence of uninsured motorists. Hit and Runs: Collision coverage will help to repair damages if the driver is not found. Another point to verify with your insurance agent is how the collision coverage applies in a hit and run incident.

Comprehensive Coverage:

While Collision covers damages from collisions caused by you or others, comprehensive covers everything else other than a collision. You can buy only collision or comprehensive coverage but typically both are sold together. If you are leasing or financing a car the leasing company will insist on you having both comprehensive and collision coverage. Comprehensive coverage typically pays for the following: (Important to check with the insurance company for finer detail as each insurance company differs)

- Fire

- Theft

- Vandalism

- Falling objects like a tree branch, or a rolling boulder.

- Civil disturbance, riots.

- Weather-related- Hurricanes, Tornados, hail damage

- Animal-Related. Ex. Deer hitting your car on the highway or running into livestock.

- Broken or shattered windows, windshields.

If you live in an area where theft is high, park the car on a street instead of a garage, drive a car which is a thief magnet, drive a lot of miles for work, live in farm country where the chances of run-ins with livestock is high, or deer encounters are common definitely go in for comprehensive coverage. In case of a qualifying incident, the insurance company will pay up to the actual cash value of the car minus the deductible which you have to pay. Choose the right deductible which you can pay at all times. Keep it high enough to reduce premiums and low enough so you can pay it always.

How to decide if Florida Comprehensive Collision Coverage is not needed?

- If you have fully paid for the car then coverage is optional.

- Check the blue book fair market value, to determine the cash value of the car.

- If you cannot easily pay to repair or replace out of pocket then you need coverage.

- If the market value of the car is less than the annual premium paid for comprehensive and collision multiplied by ten, it may not be worth the while to get this coverage. ( This is a metric given by the Insurance Institute to determine coverage necessity. ) Discuss with your insurance agent.

- Deductible and the current value of the car is the most important factor to determine the need for coverage. If the current cash value is so low that if the car is totaled, after paying the deductible and factoring in the premiums paid you will only get less than 10% of the value, you are better off not buying this coverage.

- Depreciation reduces the value of the car rapidly. A 5-year-old car is typically worth less than 40%.

Questions to ask with Insurance company/agent when you compare rates for Comprehensive Collision Coverage:

- How many days of auto rental is covered in case of an accident

- In case of aftermarket installations like GPS, LoJack, etc. is the full cost reimbursed?

- Hit and Run – How will the expenses be treated to repair/replace?

- The fine print of each insurance policy so apples to apple comparison can be made.

- Discounts for bundling Home/renters and Auto Insurance.

Gap Insurance:

If an expensive car got totaled in an incident, for which the auto loan is still being paid the comprehensive collision coverage only pays the actual cash value which might be lower than the loan amount due. “Guaranteed Auto Protection” or GAP coverage will help pay the difference. This difference in value is due to depreciation. The minute a car is driven off the dealership it depreciates by 10%. Typically after 5 years of ownership, a car is worth only less than 40% of the actual value. GAP Insurance should be considered if:

- The car is brand new and expensive, but your down payment is small.

- You drive a lot of miles and or accident prone.

- Evaluate how fast the car depreciates.

- If leasing, GAP Insurance will be included in the contract for a fee.

- If considering, be sure to ask to what extent GAP Insurance pays the difference.

- GAP insurance can be purchased separately from large insurance carriers.

Glass/Windshield:

Another advantage of having comprehensive coverage is that Florida Statute 627.7288 mandates the free replacement of damaged windshield without any deductibles by auto insurers. It is not only 100% free but also gives total discretion to choose the business which repairs or replaces the windshield provided it is a reputed business. If you have only the minimum mandated Florida auto insurance coverage then you will have to bear the expenses of repairing or replacing the windshield yourself. How to tell if your windshield needs only repair and not a replacement?

- The damaged area in your line of sight or hampering vision?

- Is the damage only chipping or bigger than a dollar bill?

- Are there more than three chipped areas?

- Is damage confined to the edge of windshield?

- If you have been in an accident it will be wise to replace the windshield.

Please be aware that you can get a ticket if you are seen driving with a windshield that is not safe. The discretion lies with the police officer. If pulled over for this you will have 30 days to fix the windshield and mail the proof of repair/replacement to the county clerk where you were fined. Your car can be declared unsafe to drive and might have to be towed at a significant cost to you. Fix a chipped or cracked windshield immediately.

Uninsured/Underinsured Motorists Coverage:

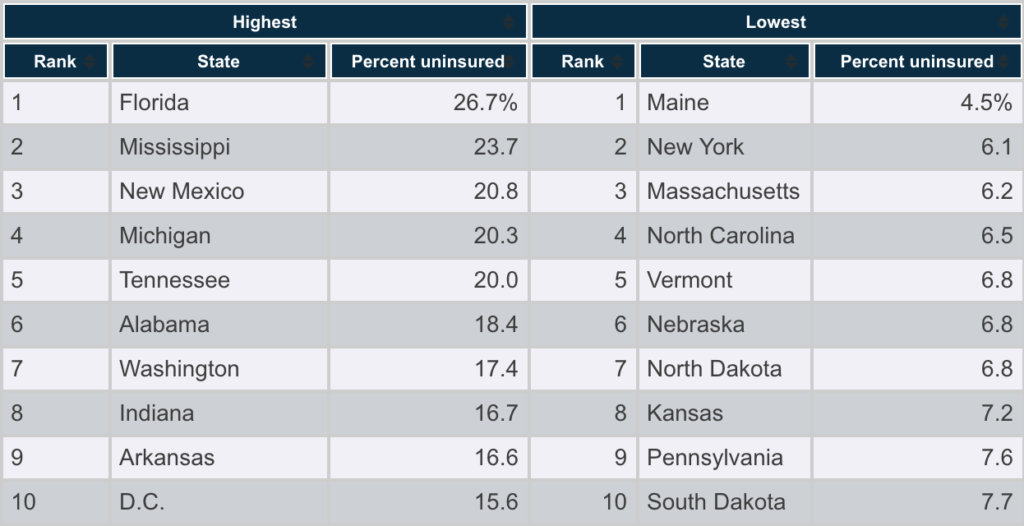

Considering one in five drivers in Florida is uninsured/underinsured this coverage is important so that one is adequately protected financially in an incident which is caused by the fault of an uninsured/underinsured motorist. According to the Insurance Information Institute, Florida has the highest uninsured motorists at 26.7% as of 2015. This insurance typically pays medical bills if there are other people in the car or lost wages after the limits of a minimal policy. This coverage is essential in Florida:

- Since the person at fault does not have to carry mandatory Bodily Injury Insurance.

- Because of this, even if someone has BI, it will not help unless UM coverage is bought along with it.

- Carrying BI helps pay bills if at fault, but will not pay BI caused by Uninsured motorist to self.

So How Much Coverage is essential?

- It is recommended to have the same amount of coverage for Bodily Injury Liability.

- The minimum is $25,000.00.

- Recommended is $100,000.00.

- Discuss the actual amount with the insurance company or agent.

- Ask for stacked and Unstacked UM coverage details. Stacked UM costs more, but you get more coverage.

Stackable UM Coverage simply stacks up UM coverage on multiple cars in one claim. So if there are 3 cars in the policy, the total sum of all 3 cars can be claimed in a qualifying incident. In Florida, if you opt for bodily injury liability insurance, as per law, the insurance company is required to also provide Uninsured Motorist coverage unless it is expressly rejected by the buyer. Florida Statute 727.727(1) reads: No motor vehicle liability insurance policy which provides bodily injury liability coverage shall be delivered in this state with respect to any specifically insured or identified motor vehicle registered or principally garaged in this state unless uninsured motor vehicle coverage is provided therein or supplemental thereto for the protection of persons insured thereunder who are legally entitled to recover damages from owners or operators of uninsured motor vehicles because of bodily injury, sickness, or disease, including death, resulting therefrom. However, the coverage required under this section is not applicable when, or to the extent that, an insured named in the policy makes a written rejection of the coverage on behalf of all insured parties under the policy.” “Uninsured drivers create risks for themselves and for all drivers, and that means purchasing just the minimum amount of required coverage may not be enough,” says Lynne Christian, Florida representative for the I.I.I. “Purchasing uninsured/underinsured motorist coverage will pay for medical expenses and lost wages after the limits of a minimal policy are paid out.” Top 10 Highest and Lowest States by Estimated Percentage of Uninsured Motorists, 2015 (1)  https://www.iii.org/fact-statistic/facts-statistics-uninsured-motorists#Top 10 Highest and the Lowest States by Estimated Percentage of Uninsured Motorists, 2015 (1)

https://www.iii.org/fact-statistic/facts-statistics-uninsured-motorists#Top 10 Highest and the Lowest States by Estimated Percentage of Uninsured Motorists, 2015 (1)

Bodily Injury Liability Insurance (BI) Coverage:

BI protects an injured person if the insured person is at fault causing a serious injury. This coverage helps pay the liability of the insured person to cover the damages of people injured in an accident. BI will pay monetary compensation for injuries incurred up to the covered amount. This is an optional coverage unless convicted of DUI. But it is recommended coverage for the following reasons:

- In case of an at-fault accident, this coverage will protect personal assets and will pay damages for sustained injuries as a result of the negligence. It can apply to anyone who is involved in a crash where the fault is of the insured person.

- It will cover other people living with the insured, who are also on the policy if they caused an accident in another car. It will also apply when others drive the insured person’s car and cause an accident.

- BI will pay for attorney costs if sued for monetary compensation for injuries caused by the fault.

- Uninsured or Under-Insured Motorist coverage (UM) cannot be bought unless BI coverage is also purchased.

Recommended BI coverage Limits: The Financial Responsibility Law of Florida has a requirement of $10,000 and $20,000 per accident, which is inadequate. It is recommended to have $100,000 per person and $300,000 per incident. Please note, UM insurance cover limits should match the same amount as the BI policy.

SR-22:

SR-22(Safety-Responsibility) is a proof of insurance document verifying that someone has auto insurance with BI and PDL. This document is prepared and filed by the insurance company with the Department of Motor Vehicles.(DMV) It is required when a driver seeks reinstatement of driver’s license after a DUI conviction, reckless driving, driving without insurance, or other moving violations that resulted in a suspension of driving privileges. Depending on whether a person owns a vehicle or not Owner-22 or non-owner-22 is filed as required. SR-22 is needed for 5 years after a DUI conviction. If the policyholder does not pay the premiums, SR-22 is canceled and an SR-26 is filed with the DMV. The policy holder’s license is suspended until a new SR-22 is filed by the insurance agent or company.

FR-44, DUI:

An FR-44 is required if a person is convicted for driving under the influence.(DUI) This document is proof of purchase of increased BIL/PDL insurance coverage of $100K/300k/50K. Filing FR-44 to the DMV is mandatory for 3 years from the original suspension date. The FR-44 will be submitted by the insurance agent or company.

Car Rental, Travel Expense, Emergency Roadside Assistance

Car Rental Coverage:

This coverage helps pay the cost of a car rental when the car is being repaired from a qualifying incident which is covered by comprehensive collision Insurance. crashing into a wall, damage from vandalism or a branch falling on the car, etc. This coverage can only be availed with comprehensive collision coverage. For a monthly coverage cost ranging from $.1.50 to $100.00, this is a must-have add on to your collision coverage. There is a per day, per incident limit. For ex. $30.00/day, the 900.00/incident option lets one rent a car at 30.00 per day up to $900.00. Depending on the car driven and the city rates vary. But it is a must have since paying out of pocket is always more expensive. Discounts are also given by car rental companies when your car is being repaired. Renting a similar car being repaired is allowed but keep in mind the duration needed to repair the car and choose accordingly. Discuss with the insurance company coverage for a minimum of 10 days to 2 weeks to get a standard quote to compare easily. Two Options:

- Reimbursement – When you rent a car of your own choice, you pay the cost upfront up to the limit allowed; the insurance company will then reimburse the cost.

- In Network – Rent a car within the insurance company’s business affiliates, the insurance company will directly pay the provider up to the limit.

Important to Note:

- This coverage is available only when your car is being repaired for a covered incident under comprehensive collision coverage.

- It is not applicable when the car is in the body shop for regular maintenance or repairs, and also vacation/recreational rentals.

- It does not pay for fuel or security deposit. Only rental is covered.

- Your comprehensive collision coverage applies when you rent another car so you do not have to buy extra coverage for the rental car.

Travel expense coverage:

This will pay for food, transportation, and hotel expenses if your vehicle is disabled in an incident covered by your comprehensive or collision insurance more than 50 miles from your home. Check with the insurance co. if this coverage is offered. This feature is not as popular as the rental coverage. If your lifestyle or work has plenty of driving it is worth having this optional coverage.

Emergency Roadside Assistance Coverage:

Running out of gas, flats, being locked out, engine failure, stuck wheels, etc., these are some of the emergencies that are covered. This is also called towing and labor coverage and provides the following services when needed:

- Towing

- Battery/Jumpstart service

- Fuel supply

- Locksmith

- Flat repair

Coverage rates and options vary from each insurance company. So ask for detailed information as to limits, exclusions, and covered services when you shop for this coverage. Due to negotiated rates, it is cheaper to get services through the insurance company rather than call independent providers. When you are in an emergency you have to call a pre-determined number to get service 24 hours which is very convenient. Obviously, you do not want the hassle of finding a local provider especially if it is night time and unknown locales. The cost of this coverage is negligible and worth having especially if you do not belong to any automotive or travel clubs like AAA. Checklist: Use the information to make a checklist of questions, comments under different coverage options to get the cheapest Florida auto insurance with optimum coverage.

- You will not forget anything when you discuss with the insurance agent.

- Gives you apples to apples comparison of Florida auto insurance quotes.

- Easy to perform what-if analysis.