Introduction

If you've ever financed or leased a car, you've probably heard the horror stories: someone gets into an accident, their car is totaled, but they still owe thousands more on their loan than what insurance covers. This nightmare scenario is exactly what auto gap insurance is designed to prevent.

With car values dropping faster than ever in 2024—especially for electric vehicles—and loan balances staying stubbornly high, more drivers are finding themselves "underwater" on their auto loans. Whether you're shopping for your first car in Texas, upgrading your ride in California, or dealing with New Jersey's sky-high insurance rates, understanding gap coverage could save you from financial disaster.

I've put together this comprehensive guide to help you navigate everything about gap insurance: what it actually does, when you really need it (and when you don't), how much it costs, where to buy it, and what alternatives might work better for your situation.

Auto Gap Insurance Fundamentals

What Gap Insurance Actually Means

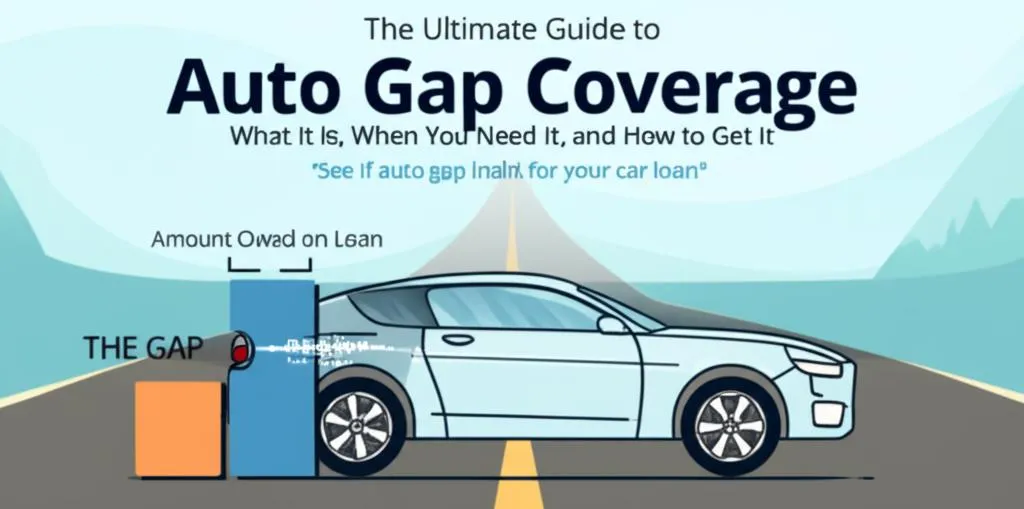

Auto gap insurance—which stands for Guaranteed Asset Protection—is like a financial safety net for anyone financing or leasing their vehicle. Think of it as backup coverage that kicks in when your regular car insurance falls short.

Here's the thing: your standard auto insurance only pays what your car is worth today, not what you still owe on it. Gap insurance covers that difference, so you're not stuck making payments on a car you can no longer drive.

How This Actually Works in Real Life

Let's say you bought a brand-new SUV for $35,000 last year. You put down $2,000 and financed the rest. Fast-forward 18 months: you're hit by an uninsured driver, and your SUV is completely totaled.

Here's where things get ugly without gap insurance: - Your loan balance: $28,500 - Your SUV's current value: $22,000 - Your insurance payout: $22,000 - What you still owe: $6,500

That $6,500 shortfall? That's money you'd have to come up with out of pocket—for a car you can't even drive anymore. Gap insurance would cover that entire amount.

Breaking Down the Insurance Jargon

- Actual Cash Value (ACV): What your car is actually worth right now, after depreciation hits

- Loan/Lease Payoff: The total amount you still owe when disaster strikes

- Deductible: What you pay upfront when filing a claim (some gap policies help with this too)

- Total Loss: When your car is so damaged that fixing it costs more than it's worth

Gap Insurance vs. Your Regular Coverage

Your collision and comprehensive coverage are great, but they're only designed to pay your car's current market value. They're not concerned with how much you still owe on your loan—that's between you and your lender. Gap insurance bridges that potentially expensive gap.

Legal Requirements and State Regulations

How Different States Handle Gap Insurance

Every state has its own rules about gap insurance, and some have gotten pretty specific about protecting consumers:

New York limits how much dealers can charge for gap waivers, essentially capping costs at reasonable levels.

California has cracked down hard on gap insurance practices, especially protecting military servicemembers from having gap insurance costs rolled into their loans. They've also mandated clearer disclosures about what coverage actually includes.

Colorado just updated their rules in 2024, raising the maximum allowable fee for gap waivers to either 4% of your loan amount or $600—whichever is higher.

Here's a quick breakdown of recent state changes:

| State | New Rules | When It Started |

|---|---|---|

| Colorado | Max fee now 4% of loan or $600 | 2024 |

| Texas | Max 5% of loan amount; must be optional | 2024 |

| Minnesota | No gap waivers for cars under $5,000 | 2024 |

| California | Stricter pricing and disclosure requirements | Recent years |

What's Required vs. What's Optional

Here's some good news: in most states, gap insurance is completely optional. Texas, for example, specifically prohibits lenders from making gap insurance a requirement for getting your loan approved.

However, some states like New York require lenders to at least offer gap coverage if they're going to hold you responsible for any loan shortfall after a total loss.

Know Your Rights

It's crucial to understand the difference between gap insurance (an actual insurance policy) and a gap waiver (where your lender agrees to forgive any shortfall). Different rules and protections apply to each, and some are only available to original owners of newer vehicles.

When Gap Insurance Is Necessary

The Reality of Car Depreciation

Let's be honest about what happens to your car's value the moment you drive it off the lot. According to industry data, here's the painful truth:

| Year After Purchase | How Much Value You Lose | What's Left |

|---|---|---|

| Year 1 | 16% | 84% |

| Year 2 | 12% more | 72% |

| Year 3 | 11% more | 61% |

By the time you've owned your car for three years, it's lost 39% of its original value. Electric vehicles face even steeper drops—sometimes losing nearly half their value in three years due to rapidly improving technology and changing incentives.

When You're Most at Risk

You're definitely in the danger zone if: - You financed a new luxury car, truck, or EV with little money down - You took out a long-term loan (72+ months) - You bought a vehicle type known for quick depreciation

You're probably safer if: - You bought a reliable model with strong resale value (think Toyota Corolla) - You made a substantial down payment - You're financing a used car at or near its market value - You chose a shorter loan term

The sobering statistic: More than 11% of all auto loans involve negative equity, with borrowers owing an average of $5,073 more than their new cars are worth, and $3,284 more on used vehicles.

Your Personal Risk Assessment

Most people financing new cars will be "underwater" on their loans for at least two to three years. If you put down less than 20% or took a loan longer than 60 months, you're almost guaranteed to need gap coverage initially.

Cost Analysis and Value Proposition

What You'll Actually Pay

The cost difference between providers is dramatic, so pay attention here:

From Insurance Companies (per year): | Provider | Annual Cost | |------------|-------------| | Progressive| ~$60 | | State Farm | ~$46 | | USAA | ~$51 | | Allstate | ~$90 |

Most insurance companies charge between $20-$100 per year, and you typically only need coverage for two to three years.

From Dealerships: - One-time cost: $400-$700 (sometimes up to $1,500) - Usually financed into your loan (meaning you pay interest on it too)

The Real Math

Let's say you need gap coverage for three years: - Insurance company route: $60/year × 3 years = $180 total - Dealership route: $600 upfront (plus interest if financed)

The dealership option often costs 100-250% more than buying through your insurance company.

Regional Price Differences

Insurance costs vary significantly by location. In New Jersey, for instance: - Average total auto insurance: $2,797/year - Adding gap coverage ranges from $30 (Travelers) to $95 (Farmers) - Progressive charges about $71 for gap coverage

Is It Worth It?

Gap insurance makes financial sense if you're financing 80-90% of your vehicle's value. It's especially valuable for high-depreciation models and situations involving small down payments with longer loan terms.

Purchasing Options and Process

Where to Buy Gap Insurance

You have three main options, each with distinct pros and cons:

Insurance Companies - Add it to your existing policy - Pay annually - Cancel anytime - Usually the cheapest option

Dealerships - Available at time of purchase - Can be rolled into your loan - Convenient but expensive - Harder to cancel later

Credit Unions and Banks - Often available at loan closing - Competitive rates - May allow adding within the first year

What Major Providers Offer

Progressive: You can buy it through them directly or through the dealership, but only if you're financing your vehicle.

AAA: Requires you to have collision and comprehensive coverage. You can call to cancel once your loan balance drops below your car's value.

Credit Unions (like MHVFCU): Often offer gap coverage at loan closing or within the first year for around $325, which can be paid upfront or financed.

What Gap Insurance Covers (And What It Doesn't)

What's Covered: - The difference between your car's value and loan balance if it's totaled or stolen

What's NOT Covered: - Normal wear and tear - Mechanical breakdowns - Routine maintenance - Late payment fees - Previous damage - Your deductible (unless specifically stated)

When to Cancel Early

Here are the top five reasons to drop gap coverage before your policy expires: 1. Your loan balance is now less than your car's value 2. You made a large principal payment 3. You paid off the loan early 4. You refinanced at a much lower balance 5. Your car's depreciation has leveled off

Consumer Experiences and Common Issues

Real Problems People Face

Based on consumer complaints and industry data, here are the most common gap insurance frustrations:

Claims Processing Headaches - Multiple requests for the same paperwork - Delays that stretch for months - Surprise "high mileage" deductions that weren't clearly explained - Claims denied because collision/comprehensive coverage lapsed

Contract Confusion - Policies that don't cover the deductible as expected - Surprise limits on total payouts - Misunderstandings about what expenses are included - Fine print that contradicts what was promised

Fraud and Service Issues - Some dealerships charged for gap insurance but never actually bought the policy - Difficulty reaching customer service - Disputes over claim settlements - Poor communication about claim status

According to industry data, 65.2% of auto insurance complaints involve claim handling issues, with delays being the top problem at 22.2%.

| Problem Type | % of Complaints | Top Specific Issue |

|---|---|---|

| Claim Handling | 65.2% | Processing Delays |

| Settlement Dissatisfaction | 12.2% | Low Payouts |

Gap Insurance Alternatives

Other Protection Options

Loan/Lease Payoff Coverage - Works similarly to gap insurance - Usually caps payouts at 25% above your car's value - Often cheaper than traditional gap insurance - Good for moderate negative equity situations

New Car Replacement Coverage - Pays extra above your car's actual value (often 20% more) - Helps you afford a comparable replacement vehicle - More expensive than gap insurance - Better for people who want to upgrade rather than just clear their debt

Self-Insurance Strategies Instead of buying coverage, you could: - Make a larger down payment upfront - Choose shorter loan terms - Buy vehicles with stronger resale values - Refinance when your loan-to-value ratio improves

Comparing Your Options

| Coverage Type | Pays Full Gap? | Cost Level | Best For |

|---|---|---|---|

| Gap Insurance | Yes | Moderate | High negative equity |

| Loan/Lease Payoff | Up to 25% ACV | Lower | Moderate negative equity |

| New Car Replacement | No, but adds value | Higher | Those wanting to upgrade |

| Self-Insurance | N/A | Upfront | Lower risk situations |

Making the Right Choice

If you're significantly upside-down on a long loan with minimal down payment, traditional gap insurance offers the most comprehensive protection. If your loan-to-value ratio is improving or you made a substantial down payment, less expensive alternatives might work better.

Always weigh the cost against your specific risk level and financial situation.

Conclusion

Gap insurance serves as crucial financial protection for millions of American car buyers who face the reality of rapid vehicle depreciation combined with high loan balances. With state regulations evolving rapidly—including new consumer protections in California, Colorado, and Texas—staying informed about your options has never been more important.

The key takeaways? Shop around between insurers and dealers (insurers almost always win on price), read the fine print carefully, and understand your state's specific consumer protections. Don't automatically assume you need gap coverage—analyze your actual risk based on your down payment, loan term, and vehicle type.

For many people, gap insurance provides invaluable peace of mind at a reasonable cost. For others, alternatives or self-insurance strategies make more sense. The important thing is making an informed decision based on your specific situation rather than just accepting whatever the dealer offers.

Remember, a well-informed choice today can save you thousands if disaster strikes tomorrow.

References

- Allstate. (2022, May). Gap Insurance Coverage.

- Car and Driver. (2023, July 6). How Does Gap Insurance Work After a Car is Totaled?

- Colorado General Assembly. (2024). Colorado GAP Waiver Legislation Changes

- Insurance.com. (2024, May 14). Gap Insurance vs. Loan/Lease Coverage vs. New Car Replacement Insurance

- Kelley Blue Book. (2025). Vehicle Depreciation Rates

- Mid-Hudson Valley Federal Credit Union. (2025). Understanding Guaranteed Auto Protection (GAP) Insurance

- National Association of Insurance Commissioners. (2024). Consumer Insurance Search and Complaint Data

- Progressive. (2025, May). Buying Gap Insurance

- Texas Department of Insurance. (2024, Oct. 14). Gap Insurance Consumer Tips

- USAA. (n.d.). Car Replacement Assistance

- Zutobi. (2024, Dec. 13). Motoring Depreciation UK and US Report

- CNET. (2022, Sep. 3). Best Gap Insurance Companies

For additional legislative sources, current carrier pricing, and supplementary research, please refer to the specific citations within each section.