When Your Premium Drops But Your Neighbor's Claim Gets Denied

Last month, Jennifer Chen got some rare good news: her Tampa auto insurance bill dropped $180. After three years of watching her premiums climb relentlessly, any decrease felt like a minor miracle. But her relief turned to worry when her coworker Maria shared a different story—six months fighting with her insurer over storm damage, mountains of paperwork, and ultimately, a denied claim that left her scrambling to pay for repairs herself.

Jennifer's experience captures exactly what's happening across Florida right now. The state's aggressive insurance reforms are working—but not for everyone, and not in the ways most people expected.

If you're a Florida resident, these changes are already affecting your premiums, your claims, and your coverage options. Here's what you actually need to know about where this is headed and what it means for your specific situation.

What Actually Changed (And Why It Matters to You)

They Killed the "Sue First, Ask Questions Later" System

Here's what was broken: lawyers could file tiny insurance claims, barely lift a finger, and collect thousands in fees when they won. A $500 medical claim could generate $5,000 in attorney fees. This made Florida a magnet for insurance lawsuits—and those legal costs got passed straight to you through higher premiums.

The 2023 reforms eliminated these "one-way attorney fees" for Personal Injury Protection claims. Translation: fewer frivolous lawsuits, which means lower costs for insurance companies, which should mean lower premiums for you.

What's coming next: Senate Bill 554 introduces a sliding scale for attorney fees. Lawyers only get full payment when they secure at least 80% of what they originally demanded. Get less than 20%? They get nothing. This should further discourage weak cases while protecting legitimate claims.

Your Claims Now Come with Strict Deadlines

Starting July 2025, your insurance company has to give you written damage estimates within seven days. They also have to send monthly updates on what they're doing with your claim. Miss the 90-day investigation deadline? You can skip mediation and go straight to court.

The catch: Insurance companies now have just 10 days to respond to settlement demands, or they risk immediate lawsuits. This creates pressure for quick decisions—which could work for or against you depending on your situation.

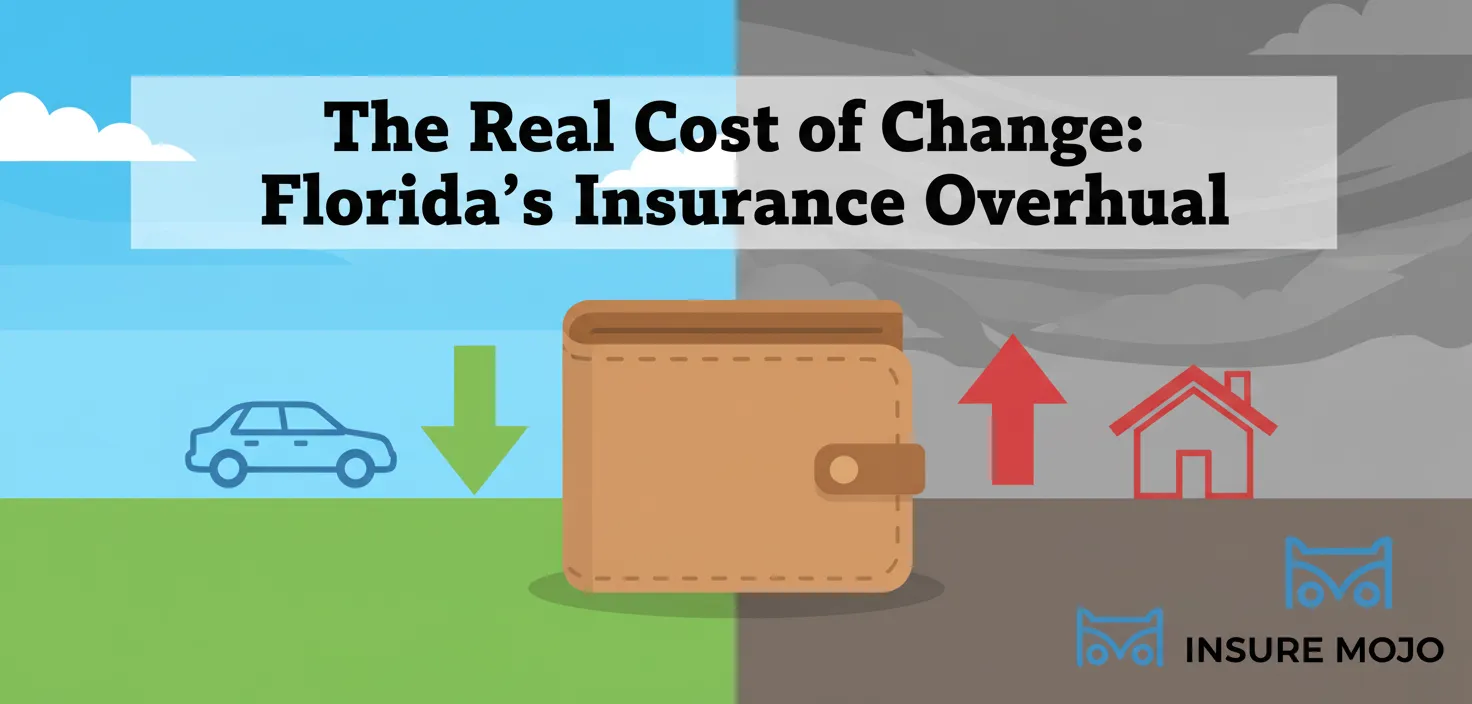

Auto Insurance Is Getting a Complete Makeover

Florida is ditching its "no-fault" auto insurance system. Right now, your insurance pays your medical bills regardless of who caused the accident. Soon, whoever causes the crash pays for everyone's injuries.

What this means for you: - Minimum coverage requirements are doubling: $25,000 per person and $50,000 per incident for bodily injury - If you're a safe driver, you could save around $350 annually - If you're high-risk, your premiums could jump 50-75% - If someone hits you, their insurance pays your medical bills (assuming they have adequate coverage)

The Good News: What's Actually Working

Lawsuits Are Plummeting

Insurance-related lawsuits dropped nearly 24% in 2024. For auto insurance specifically, frivolous PIP lawsuits have virtually disappeared. This directly translates to your premium relief.

Your benefit: Auto insurance premiums rose just 4.3% in 2024 (compared to 32% in 2023) and are projected to decrease 6.5% in 2025—the first meaningful reduction in years.

Insurance Companies Are Coming Back

Fourteen new companies have started writing homeowner's policies since 2023. When insurers voluntarily enter a market they've been fleeing, it's a strong sign that conditions are improving.

What this means for you: More competition should lead to better rates and service. Citizens Property Insurance—the state's insurer of last resort—has shrunk by nearly 50% as private companies take on policies they previously wouldn't touch.

The Reality Check: Where You're Still Getting Squeezed

Homeowner's Insurance Remains Brutal

While auto insurance improves, homeowner's premiums hit an average of $2,625 in 2025—about 40% higher than in 2022. Central Florida residents are paying even more.

The math: Many Florida homeowners now pay more for insurance than their car payment. Rate increases have slowed to 0.3% (down from double-digit spikes), but you're still dealing with years of accumulated increases.

Your Complaints Aren't Being Heard

Consumer complaints have more than doubled in five years, jumping from about 10,000 in 2020 to over 23,000 in 2024. Regulators project complaints could hit 31,000 in 2025.

The problem: Only about 5% of homeowner complaints get referred for investigation. The regulatory system splits authority between different agencies, creating gaps where legitimate grievances fall through the cracks.

Hurricane Season Could Wipe Out Progress

Florida's insurance market remains vulnerable to catastrophic losses. One bad hurricane season could quickly reverse recent premium improvements and send insurers fleeing again.

What You Should Do Right Now

For Auto Insurance

If you're switching to the new system: Start shopping now. The elimination of PIP and higher bodily injury requirements will affect everyone differently. Get quotes based on the new requirements to avoid surprises.

If you're a safe driver: You'll likely benefit from the changes. Consider raising your deductibles to maximize savings.

If you have a spotty driving record: Budget for potentially significant increases. The new system penalizes risky drivers more heavily.

For Homeowner's Insurance

Shop aggressively: With more insurers entering the market, you have options you didn't have two years ago. Get quotes every six months.

Document everything: With stricter claims processes, detailed documentation becomes crucial. Take photos, keep receipts, and respond to all insurer requests promptly.

Understand the new timelines: Your insurer has 90 days to investigate claims, but you have new rights to monthly updates and quick damage estimates.

Red Flags to Watch For

- Insurers missing the new deadlines: Seven-day damage estimates and monthly updates aren't suggestions—they're requirements

- Excessive delays in the PIP transition: If your auto insurer isn't clearly communicating the changes, start shopping

- Citizens policies that should be transferable: If you're still with Citizens despite market improvements, make sure you're not overpaying

The Bottom Line for Florida Residents

The reforms are working, but unevenly. Auto insurance is genuinely improving—you'll likely see real savings in 2025. Homeowner's insurance remains expensive, though the rate of increase has slowed dramatically.

Your biggest risks going forward are implementation hiccups during the auto insurance transition and potential hurricane losses that could trigger new rate spikes. The biggest opportunities are increased competition and clearer rules that should make it easier to hold insurers accountable.

For Jennifer Chen and millions of other Florida residents, the insurance reforms represent real progress toward a more functional market. But comprehensive affordability relief—the kind that makes insurance feel reasonable rather than punishing—remains a work in progress.

The key is staying informed and acting on the opportunities these changes create. In Florida's insurance market, passive consumers get squeezed. Active ones find ways to win.