President Trump claimed this week that illegal immigration drove car insurance premiums to record highs under President Biden, and that his immigration crackdown is now pushing them down. Economists and insurance analysts who track premium data call that false, estimating illegal immigration explains only about 0.07% of the roughly 50% rate surge that hit drivers after COVID-19.

For the average driver paying $2,144 a year for full coverage, that 0.07% works out to roughly $1.50, according to figures from Insurify and Johns Hopkins economist Michael Clemens. The far bigger forces, pandemic-era repair inflation and a spike in accident claims, added several hundred dollars to that same policy.

In a June 15 Truth Social post, President Trump blamed illegal immigration for record car insurance premiums and credited his border crackdown for the recent decline. An Associated Press fact-check and the Insurance Information Institute found no evidence for that link. Economists trace the roughly 50% premium increase since 2020 to COVID-19 repair costs, supply-chain disruption, and higher accident claims, with immigration explaining about 0.07%.

- Johns Hopkins economist Michael Clemens calls the immigration claim "pure fiction," tying it to about 0.07% of the post-2020 surge.

- Blame the COVID-19 era: repair-part inflation and a jump in accident claims pushed prices up roughly 50% from 2020 to 2024, BLS data shows.

- After peaking, full-coverage premiums fell 6% in 2025 to a $2,144 national average, according to Insurify.

- Lower your own bill by comparing quotes, raising your deductible, and confirming low-mileage discounts, levers that outweigh any immigration debate.

What Trump Claimed

The claim landed Monday, June 15, in a Truth Social post that paired a chart with a blunt accusation. Trump's graphic plotted the year-over-year change in premiums from 2021 through 2026, citing a Council of Economic Advisers analysis of Bureau of Labor Statistics data. The line climbs hard through 2023, bends downward after that, and finishes with a decline in 2026.

"Car Insurance Premiums rose to RECORD HIGHS, forcing Law-abiding American Citizens to subsidize the 'free riding' Biden Illegals," the post read. "After over a year of ZERO ILLEGAL IMMIGRATION, and our highly successful efforts to REVERSE the Biden Invasion, Car Insurance Premiums have come tumbling down."

The underlying numbers are real, because premiums did jump about 50% and have since cooled. The cause Trump assigned to them is where economists draw the line.

What Actually Raised Car Insurance Rates

Start with the pandemic, which reshaped driving in 2020. When COVID-19 lockdowns emptied the roads, drivers filed far fewer claims, and several insurers issued rebates as profits climbed. Traffic returned in 2022, and with it came more crashes, more injury claims, and a wave of distracted driving that carriers had to price in.

Repair bills did the rest, climbing faster than overall inflation for three straight years. Supply-chain breakdowns made parts and labor more expensive, so the cost of fixing a damaged vehicle outran the broader economy. Carriers passed those costs to drivers, and the Bureau of Labor Statistics logged a motor-vehicle-insurance increase of 19.2% in the year ending November 2023, with the annual rate touching 22% by spring 2024.

| Time Period | Car Insurance Price Change | Primary Cause |

|---|---|---|

| 2020 | Fell, plus rebates | Lockdowns cut driving and claims (BLS) |

| Year to Nov. 2023 | +19.2% | Repair-part and labor inflation (BLS) |

| Spring 2024 | +22.2% | Carriers recouping prior losses (BLS peak) |

| Full-year 2025 | -6% to $2,144 | Profits restored; price competition (Insurify) |

| Early 2026 | +5.9% and cooling | Costs near general inflation (BLS) |

Sources: U.S. Bureau of Labor Statistics Consumer Price Index for motor vehicle insurance (year-over-year, urban consumers), 2020 through early 2026; Insurify's 2026 report for the full-year 2025 average full-coverage premium of $2,144, drawn from rate analysis across all 50 states. The BLS index measures price changes on existing policies, while Insurify reflects quoted rates for new full-coverage policies, which is why 2025 shows a decline before the BLS index does.

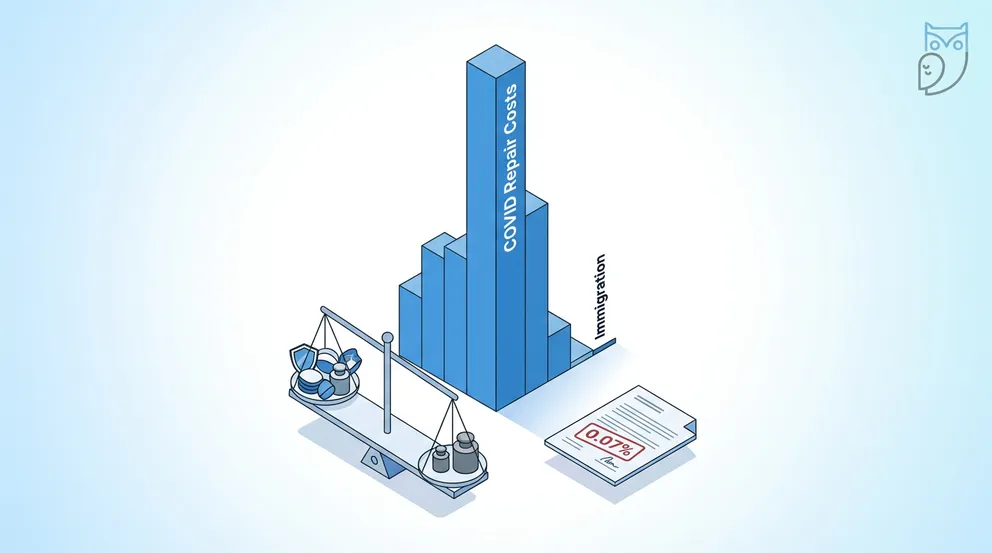

The 0.07% Reality Check

Michael Clemens, an economics professor at Johns Hopkins University and a senior fellow at the Peterson Institute for International Economics, did not hedge when the AP asked him about the post.

"This claim is pure fiction," Clemens said. "It does not arise from any study by the White House, by the auto insurance industry, or even by anti-immigration pressure groups. It has no basis in anything but inflammatory statements that juxtapose two unrelated trends."

Clemens put a number on it. The Biden-era rise in illegal immigration can explain roughly a 0.07% increase in premiums, a rounding error against the near-50% climb that BLS data recorded. On the $2,144 that the average driver now pays for full coverage, 0.07% comes to about $1.50 a year, while repair inflation and claim costs added several hundred dollars to that same bill.

One narrow link does exist. A 2023 study in the Journal of Insurance Issues found that areas with more unauthorized immigrants also have more uninsured drivers, who push up everyone else's premiums through uninsured-motorist claims. That effect surfaces only in states that bar unauthorized immigrants from getting driver's licenses, and it never approaches the scale of the pandemic shock. Drivers worried about that risk can review their own uninsured motorist coverage instead of the national immigration debate.

The White House defended the post. Asked for evidence, spokesman Kush Desai pointed to a drop in traffic fatalities, eased congestion in high-immigration cities, and the removal of more than 20,000 commercial truck drivers it said posed safety risks. Insurance analysts counter that none of those factors registers as a measurable driver of the 2021 to 2024 premium surge.

Why Rates Are Falling Now

The decline Trump highlighted is genuine, and the industry explains it without any reference to the border. After two years of steep rate hikes, insurers have returned to underwriting profit, the strongest position they have held in years. Lower claim frequency and stabilizing repair prices gave carriers room to compete on price again.

"Over the past two years, the auto insurance industry has generated an underwriting profit following the implementation of significant rate actions to offset losses," said Mark Friedlander of the Insurance Information Institute. "We are seeing average rate decreases being implemented across numerous states, as well as dividends being paid to policyholders by major auto insurers such as State Farm and USAA."

Insurify's market data backs him up, reporting that full-coverage premiums fell 6% in 2025, with 39 states posting declines and eight dropping 15% or more.

What This Means for You

Your premium reflects what insurers expect to pay to repair your car and settle claims in your ZIP code, not who crossed the border. Your driving record, credit-based insurance score, annual mileage, and vehicle repair cost shape the bill far more than any headline, and you can compare, switch, or adjust most of those factors yourself.

Location still drives big swings. Drivers in high-cost states pay well above the $2,144 national average because of local repair bills, litigation, and uninsured-motorist rates, so the smartest move is to measure your own renewal notice against that benchmark. If your premium is not drifting down in 2026, your carrier may be lagging the broader market.

What You Should Do Now

Compare at least three quotes

Rates fell 6% in 2025, yet only active shoppers capture the savings. A side-by-side quote comparison from three or more carriers shows whether your renewal keeps pace, so match the coverage limits before you judge the price.

Question your loyalty

Staying put can backfire, because some insurers charge a quiet loyalty penalty to long-tenured drivers. Ask your agent whether a fresh new-customer quote beats your current premium.

Tune the factors you control

Raise your deductible, report lower annual mileage, and claim telematics or bundling discounts where you qualify. Those levers move your premium far more than the immigration debate ever will.

Looking Ahead

The relief may not last all year. Insurify projects the national full-coverage average will tick up about 1% in 2026 to roughly $2,158, with prices rising in 35 states even as 15 keep falling. New tariffs on imported parts and vehicles are the wild card, since they could push repair costs, and premiums, higher again. The BLS index even fell 1.7% in May 2026 alone, a sign the steep declines are flattening.

Watch your renewal notice and the monthly BLS inflation report for the real signal. If parts costs climb, expect carriers to file for increases within two or three quarters, regardless of immigration headlines. Your declarations page, not a social media post, is where this year's rate swing turns into real dollars.

Frequently Asked Questions

Experts say no, not in any meaningful way. Johns Hopkins economist Michael Clemens estimates it explains about 0.07% of the roughly 50% premium increase since 2020. The Insurance Information Institute attributes the rise to pandemic-era repair costs, supply-chain disruption, and higher accident claims.

Repair and claim costs surged. BLS data shows motor-vehicle-insurance prices rose 19.2% in the year to November 2023 and peaked near 22% in spring 2024, driven by costlier parts, more accidents, and litigation.

Yes, modestly. Insurify reports full-coverage premiums fell 6% in 2025 to a $2,144 national average, and 39 states saw declines. Insurify projects a small 1% rise for 2026, so the steepest drops may be ending.

Only at the margins. A 2023 Journal of Insurance Issues study links areas with more unauthorized immigrants to more uninsured drivers, but only in states that deny them licenses, and the effect is tiny next to repair-cost inflation. Uninsured motorist coverage protects you from that risk directly.

- Insurance Journal / Associated Press - Trump Says Illegal Immigration Increased Car Insurance but Experts Say Otherwise

- Washington Times / AP Fact Focus - Trump Says Illegal Immigration Increased Car Insurance Premiums

- U.S. Bureau of Labor Statistics - Consumer Price Index, Motor Vehicle Insurance (May 2026 release)

- Insurify - Car Insurance Prices Tumbled 6% in 2025 (2026 Report)

- Insurance Information Institute (Triple-I) - Auto Insurance Trends

- Journal of Insurance Issues (2023) - Unauthorized Immigration and Uninsured Drivers